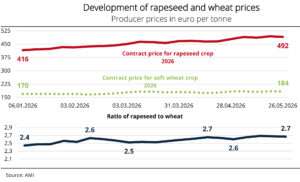

The price gap between forward contract prices for soft wheat and rapeseed from the 2026 crop has recently widened to a ratio of 1:2.7, further increasing the incentive for farmers to sow rapeseed for the 2027 harvest.

At the end of May 2026, rapeseed growers in Germany received an average of just under €492 per tonne ex farm for forward contracts for the 2026 crop, more than twice the price buyers paid for one tonne of soft wheat.

Rising energy prices resulting from geopolitical tensions in the Middle East have recently led to stronger prices on the Paris futures market, thereby also supporting producer prices for rapeseed. However, the resulting momentum was largely short-lived, with fundamental data remaining the key factor influencing medium-term market trends.

Producer prices for soft wheat from the 2026 crop also strengthened over the past few weeks, though to a lesser extent than those of rapeseed. At €184 per tonne, they were around €1.50 per tonne lower than at the same time in 2025. Current activities on the domestic market have focused on clearing warehouses and fulfilling forward contracts, with new business remaining the exception.

All things considered, the current price ratios clearly suggest that winter rapeseed is the better option. Fundamental data are stable and there are no signs of any major supply bottlenecks. Regional weather risks continue to exist but are cushioned across the EU by expansions of the production area.

This means that, in general, winter rapeseed continues to offer attractive economic prospects for crop rotation and remains a competitive option for the 2026/27 season.

Rapeseed prices offer farmers incentive